Apple And Lenovo Buck PC Market Decline Ahead of Windows 10 Release – IDC

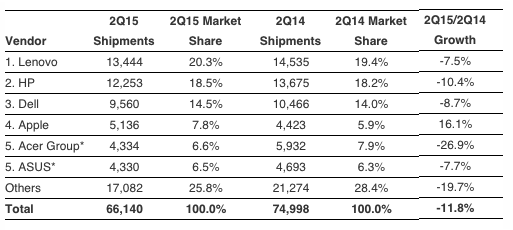

Worldwide PC shipments totaled 66.1 million units in the second quarter of 2015 (2Q15) according to the International Data Corporation (IDC) Worldwide Quarterly PC Tracker. This represented a year-on-year decline of -11.8%, about one percent below projections for the quarter.

The slow PC shipments were largely janticipated as a result of stronger year-ago shipments relating to end of support for Windows XP as well as channels reducing inventory ahead of the Windows 10 release. In addition, weaker or changing exchange rates for foreign currencies have effectively increased PC prices in many markets, thereby reducing purchasing power and also complicating investment planning.

“Although the second quarter decline in PC shipments was significant, and slightly more than expected, the overall trend fits with expectations,” says Loren Loverde, Vice President, Worldwide PC Trackers & Forecasting. “We continue to expect low to mid-single digit declines in volume during the second half of the year with volume stabilizing in future years. We’re expecting the Windows 10 launch to go relatively well, though many users will opt for a free OS upgrade rather than buying a new PC. Competition from 2-in-1 devices and phones remains an issue, but the economic environment has had a larger impact lately, and that should stabilize or improve going forward.”

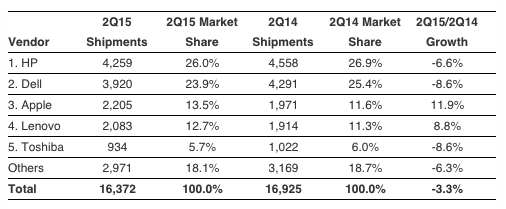

“The U.S. market was in line with forecasts, declining -3.3% from a year ago, after avoiding the global market declines over the past five quarters. Soft retail demand, short term weakness from inventory reductions, some cannibalization from competing devices, and low demand for large commercial refreshes are among the factors that reduced PC shipments,” observes Rajani Singh, Senior Research Analyst, Personal Computers. “Nevertheless, moving forward, we expect a healthy second half as inventory and purchase decisions pick up following the launch of Windows 10. Emerging product categories will remain a bright spot as attention shifts to convertibles and Chromebooks in the commercial as well as consumer segments.”

Regional Highlights

United States With shipments totaling nearly 16.4 million PCs in 2Q15, the U.S. market shrank -3.3% from the same quarter a year ago. Although most vendors saw volume decline, gains from Apple and Lenovo helped limit the overall decline. A tough year-on-year comparison contributed to a decline in desktop shipments, while portable PCs shipments continued to grow.

Europe, Middle East, and Africa (EMEA) In EMEA, weakening demand and high inventory levels inhibited sell-in, driving results below expectations. Vendors continued to clean stock ahead of the back-to-school season and Windows 10 launch. Moreover, unfavorable exchange rates led to increasing prices and continued to affect demand both in the business and consumer spaces. The commercial market also faced a difficult year-on-year comparison with 2Q14, when the end of support for Windows XP boosted sales.

Asia/Pacific (excluding Japan) China was impacted by excess commercial notebook inventory from earlier quarters as the anti-corruption campaign continues to suppress commercial spending. Currency fluctuation also remained a key factor in many countries in the region, contributing to lower demand. Nevertheless, volume was close to expectations, reflecting a slight decline in growth from prior quarters.

Japan continued to see low growth as the weak Yen contributed to a difficult market. The Japanese PC market faced a particularly difficult comparison to year ago shipments that were boosted by the end of support for Windows XP and also changes to Japan’s tax code. As the market responds to these shifts and managing inventory, Yamada Denki (one of Japan’s major electronics stores) announced the closure of unprofitable stores in both urban and rural markets.

Vendor Highlights

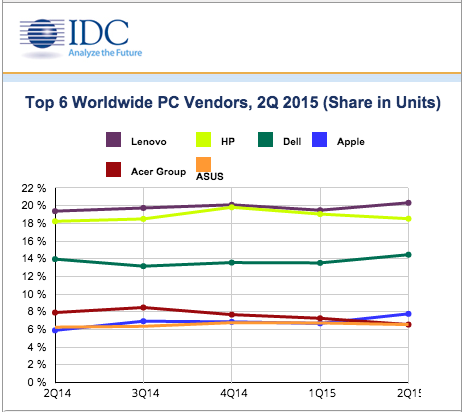

Lenovo held onto the top position with shipments of 13.4 million units. Volume was up 1% from the prior quarter, but down -7.5% from the prior year. The vendor continued to aggressively court expansion outside of Asia/Pacific, leading to share gains in the U.S. and EMEA.

HP remained the number 2 vendor, but saw shipments decline -10.4% from a year ago. Slowing business demand and inventory control of entry notebooks contributed to the dip. While most of the slowdown was from outside of the U.S., the vendor also saw its U.S. volume contract nearly -7%.

Dell came in at number 3, shipping more than 9.5 million units and registering a year-over-year decline of -8.7%. Strong results in 2Q14 contributed to a poor year-over-year comparison. Stronger performance in Asia/Pacific and EMEA were offset by slower growth in the U.S.

Apple continued to outperform other vendors, with growth of 16.1% globally. The vendor has largely avoided the price competition affecting other players and may be benefitting from some of the uncertainty around the launch of Windows 10, along with refreshed products like the 12-inch MacBook and a relative concentration of shipments in the U.S.

Acer continued to see growth in Chromebooks with more models introduced. However, the vendor also struggled with the larger pullback in the market, particularly in EMEA where it had seen a rebound in mid-2014. The vendor ended 2Q14 with a volume of 4.33 million, a significant decline from the prior quarter and year ago volumes.

ASUS was statistically tied* with Acer for the number 5 position. ASUS has also been affected by currency factors and inventory management, but strong growth in the U.S. boosted overall results.

Top 5 Vendors, Worldwide PC Shipments, Market Share, and Year-Over-Year Growth for the Second Quarter of 2015

(Preliminary) (Shipments are in thousands of units)

Source: IDC Worldwide Quarterly PC Tracker, July 9, 2015

* Note: IDC declares a statistical tie in the worldwide PC market when there is less than one tenth of one percent difference in the revenue share of two or more vendors.

In addition to the table above, an interactive graphic showing worldwide PC market share for the top 5 vendors over the previous five quarters is available here. The chart is intended for public use in online news articles and social media. Instructions on how to embed this graphic can be found by viewing this press release on IDC.com.

Top 5 Vendors, United States PC Shipments, Market Share, and Year-Over-Year Growth, Second Quarter of 2015

(Preliminary) (Shipments are in thousands of units)

Source: IDC Worldwide Quarterly PC Tracker, July 9, 2015

Table Notes:

• Some IDC estimates prior to financial earnings reports.

Shipments include shipments to distribution channels or end users. OEM sales are counted under the vendor/brand under which they are sold.

• PCs include Desktops, Portables, Ultraslim Notebooks, Chromebooks, and Workstations and do not include handhelds, x86 Servers and Tablets (i.e. iPad, or Tablets with detachable keyboards running either Windows or Android). Data for all vendors are reported for calendar periods.

IDC’s Worldwide Quarterly PC Tracker gathers PC market data in over 80 countries by vendor, form factor, brand, processor brand and speed, sales channel and user segment. The research includes historical and forecast trend analysis as well as price band and installed base data.

For more information, visit:

http://www.idc.com

Follow IDC on Twitter at @IDC.

Source: IDC