Smartphone Volumes Decline Slightly in 2017 Second Quarter Amid Anticipation of Strong Second Half Product Launches – IDC

According to preliminary results from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, smartphone OEMs shipped a total of 341.6 million smartphones worldwide in the second quarter of 2017 (2Q17). Coming off a higher than expected first quarter, smartphone shipments declined 1.3% from the same quarter a year ago and were down 0.8% from 1Q17.

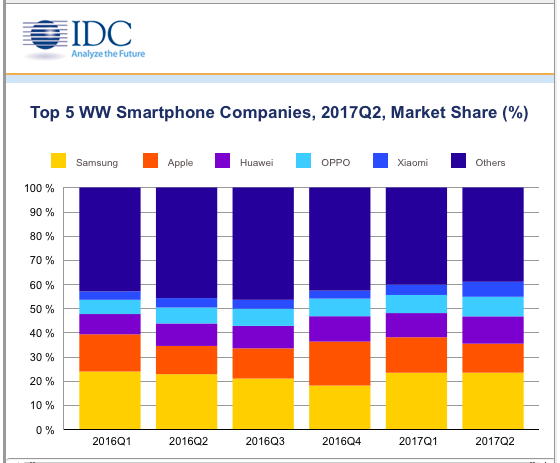

While the smartphone industry contracted slightly in the second quarter, it is worth noting that the leading vendors all saw positive shipment growth. Samsung and Apple both held shares relatively constant from the second quarter a year ago, while the other three vendors rounding out the top 5, Huawei, OPPO, and Xiaomi, all grew shares. The one change in terms of ranking within the top 5 was Xiaomi slightly outpacing vivo, but not by much.

“In my opinion, the biggest change in the second quarter is the size of the contraction among the ‘Others’ outside of the top 5 OEMs,” said Ryan Reith, program vice president with IDC’s Worldwide Quarterly Mobile Device Trackers. “It’s no secret that the smartphone market is a very challenging segment for companies to maintain or grow share, especially as already low average selling prices declined by another 4.3% in 2016. The smaller, more localized vendors will continue to struggle, especially as the leading volume drivers build out their portfolio into new markets and price segments.”

As we look toward the second half of 2017, IDC expects to see two quarters of positive year-over-year growth, leaving 2017 as a rebound year. Samsung is riding momentum from the Galaxy S8 products, with the presumed August announcement of the Note 8 right around the corner. In parallel, anticipation continues to build for the next round of iPhones that the industry expects Apple to announce in September. Outside of these two industry leaders, the companies to watch will continue to be the next three to five OEMs and how they navigate to position themselves in growing markets.

“Despite some key launches in the second quarter from some well-known players, all eyes will be on the ultra-high-end flagships set to arrive this fall,” said Anthony Scarsella, research manager with IDC’s Worldwide Quarterly Mobile Phone Tracker. “With devices like the iPhone 8, Pixel 2, Note 8, and V30 in the pipeline, the competition will be fierce come September. We expect all the key players to promote their latest and greatest flagships with an assortment of deals, bundles, and trade-in offers across a variety of channels in most key markets.”

Smartphone Company Highlights

Samsung remained the leader in the worldwide smartphone market grabbing an impressive 23.3% share and 1.4% growth. The new S8 and S8+ played an important role in the quarter as the flagship brought a new design and screen aspect ratio (18:9) to the table, which could transform the industry in the months ahead. Consumers have responded well to the edge-to-edge display, and we expect numerous other vendors to bring out similar designs heading into next year. Outside of the S8/S8+, Samsung continues to perform well at the mid-to-low end with its “A” Series and “J” Series devices. Much like Apple, all eyes will be on the next big thing as the Note 8 will look to permanently erase all memories of the Note 7 debacle from last year.

Apple shipped 41.0 million iPhones in the second quarter representing mild 1.5% year-over-year growth from the 40.4 million units shipped last year. The iPhone continues to perform well at the high end as the 7 Plus outperformed the 6S Plus from one year ago. The iPhone 7 and 7 Plus combined delivered double-digit growth at a worldwide level, which helped grow average selling prices (ASPs) by 2% despite foreign exchange headwinds. All eyes will be on the iPhone 8 come September as Apple is expected to bring new features such as a larger AMOLED display, wireless charging, and increased performance and durability. The all new model is supposed to join a new 7S, and 7S Plus come the fall.

Huawei captured the third position once again thanks to strong sales in greater China as well as in many developed European markets. The Chinese giant witnessed 19.6% year-over-year growth and improved its market share by two full percentage points compared to the second quarter of last year. Huawei’s mid-range and high-end models continue to prove successful along with the flagship P10, Mate 9, and the more affordable Honor series. Looking ahead, Huawei will still need to successfully penetrate the U.S. market at the carrier level if it wishes to surpass either Apple or Samsung at the top.

OPPO remained in the fourth position with worldwide shipments of 27.8 million units and moving its overall share up 1.5 percentage points to 8.1%. The Chinese brand continues to expand its international business, leading with many markets in Southeast Asia. During the quarter, it expanded its number of service centers in India and added its new exclusive retail outlets as well. In Thailand, OPPO continued to expand its channels and advertisements with billboards across the country. It also partnered with one of the local operators to offer the A37 for free, which directly helped to grow its customer base.

Xiaomi moved back into the top 5 worldwide with year-over-year growth of 58.9%, edging slightly ahead of vivo. Xiaomi has been very aggressive in the India market, expanding its offline presence by launching its first Mi Home store and partnering with key large format retailers to increase its retail footprint. It has also doubled the number of service centers in the past six months as it continues with its strong below-the-line marketing activities.

For more information, visit:

http://www.idc.com

Source: IDC Worldwide Quarterly Mobile Phone Tracker